Proponents: Is Venture Capital the Best Asset Class?

The Tiny Asset Class Powering the Modern Economy

Credit National Park Service

Venture capital represents less than 1% of U.S. GDP, yet it is the primary engine behind the most transformative companies in the modern economy. From the smartphone in your pocket to the rockets landing themselves on ocean platforms, VC-backed businesses account for a staggering 77% of U.S. public market capitalization and 92% of all private R&D spend. While critics focus on the failures, the data suggests that without this ‘tiny’ asset class, the 21st century would look fundamentally different.

This Week’s Focus: Venture Capital

What You’ll Understand: Favorable Viewpoints on the Venture Capital Industry

Reading Time: 14 minutes for full analysis + key takeaways highlighted throughout

Key Question: Is venture capital the best asset class?

My Take: Many investors claim that venture capital is the best asset class. In many ways, it is better than other asset classes. It produces high returns for a select few investments, driving innovation and positive externalities for society. However, there are some aspects that are hard to dismiss (covered in part 3). In aggregate, venture capital is a very good asset class, but it might not be the best.

Quick Context: This deep dive connects to my work historically on venture capital (here). New to Brainwaves? We explore the forces reshaping our world across venture capital, energy, space, economics, intellectual property, and philosophy. Subscribe here for bi-weekly deep dives plus weekly current events.

Refer a Friend - Earn These Rewards

Let’s dive in.

Venture capital has rapidly evolved and expanded throughout the last couple of decades into a full-fledged industry. Throughout its development, many of the industry’s core characteristics and the players’ fundamental properties have changed drastically to adapt to emerging trends and ultimately increase success rates.

As such, our knowledge of modern industry principles and practices may miss key developments or be fundamentally skewed by historical thinking.

The purpose of this essay today is to continue acknowledging and addressing aspects of the modern venture capital industry and any misconceptions we may have, revolving around one of the biggest overarching questions: Is venture capital the best asset class?

View part 1, part 2, and part 3 of this series.

Is venture capital truly the best asset class?

Most of the people I know who write about venture capital, in one way or another, are pretty adamantly on one side of the aisle or the other (i.e., they really love VC or really despise it).

One of those people I read frequently is Packy McCormick at Not Boring. If you can’t tell from any of his articles (here, here, here, or here), he writes about VC often and is a strong proponent of it. Why?

The Proponents

The proponents of venture capital being the best asset class list a wide variety of reasons, the main of which are:

Venture capital fund returns (as an average across the asset class) are higher than those of other asset classes

Venture capital funds a large portion of innovation in the U.S.

Venture capital is the best situated to embrace variance in returns

Venture capital is able to fund the wildest ideas in the world

The venture capital industry builds upon itself over time

The failure of one company’s returns doesn’t necessarily spell failure for the fund’s returns

Venture capital investors have an active involvement in value creation

Venture capital can help social and economic impact

Proponents’ Rationale #1: Venture Capital Fund Returns Are Higher Than Those of Other Asset Classes

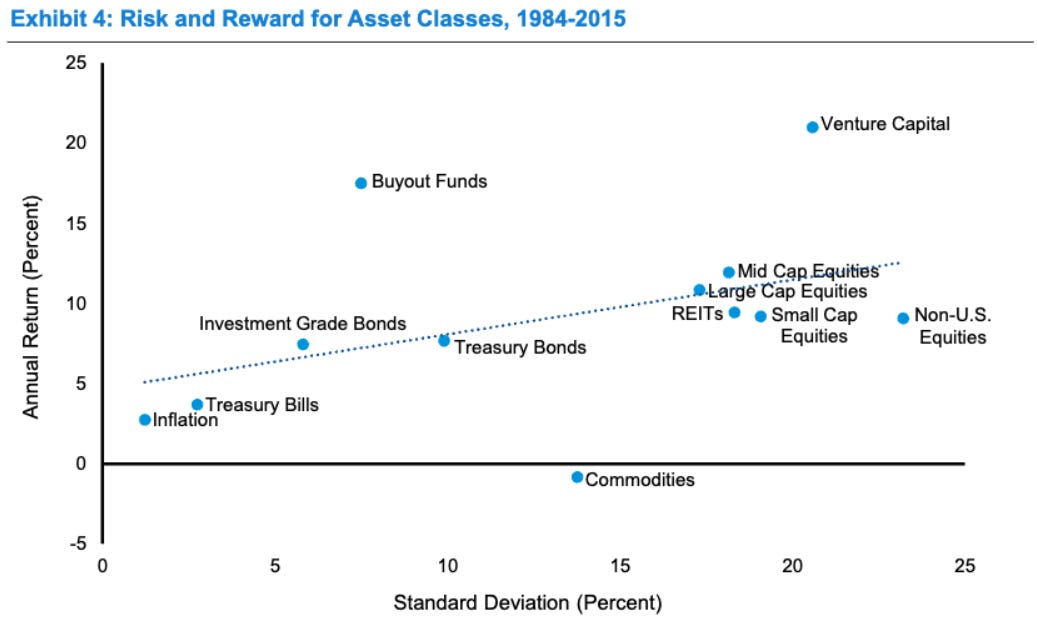

In one of Packy’s recent articles, he uses the following graph from a 2015 study comparing private and public company investments by researchers at the University of Virginia. The results speak for themselves:

Credit Not Boring

As you can see, given its risk level, venture capital aggressively outperforms its peers. Packy explains that the data isn’t perfect, but is directionally correct. Depending on the time horizon you use and whether or not you’re using risk-adjusted returns, venture capital may or may not be the best-performing asset class.

If you’re like me, you don’t always trust one source, so here are other sources that prove a similar point (here, here, here, and here).

There’s virtually no other asset class capable of providing returns of 50%+ annualized IRR over a 10-year fund cycle. To be clear, not every venture capital fund can hit this level of returns; it’s a select few (a good IRR is around 20%, per the graph above).

Why does venture capital return this high? It’s a combination of factors, mainly the risk and return profile, diversification, and the types of companies invested in. Don’t worry, we’ll discuss each of these points further.

Proponents’ Rationale #2: Venture Capital Funds a Large Portion of Innovation in the U.S.

What isn’t in doubt is that venture capital funds a large portion of the innovation in our society. As we’ll touch on later, whether the company is a winner or a loser, there are benefits to innovation in every scenario.

As writers from Adams Street Capital explain, venture capital is a relatively tiny asset class in terms of total dollars, representing less than 1% of the U.S. GDP, yet it is the primary engine behind the most transformative companies in the U.S. economy. They elaborate:

Venture capital firms have a multi-decade history of facilitating innovation. Four of the five largest public companies by market capitalization at the end of 2022 trace their roots to VC funding. According to the National Venture Capital Association, half of all US public companies benefited from venture investment, while VC-backed businesses make up about 77% of US public market capitalization, 81% of total patents granted by the US Patent and Trademark Office, and 92% of research and development (R&D) spend. Since 2001, 53% of all initial public offerings (IPO), and 70% of tech companies going public had VC backing, according to Professor Jay Ritter at the University of Florida.

Traditional corporations often focus on incremental innovation—making an existing product 1-10% better—to protect their quarterly earnings. Venture capital firms fund disruptive innovation—companies that make existing products and solutions obsolete.

Venture capitalists often take on technical risks that public markets won’t touch, often because of their speculative nature. For example, in 2026, venture capital is the dominant funder of commercial nuclear fusion, quantum computing, and synthetic biology.

Venture capital doesn’t just fund products; it creates entire industries that didn’t exist a decade ago.

The Internet Economy: Google, Amazon, Meta

The Space Economy: SpaceX, Relativity Space, Stoke Space

The Modern Energy Grid: Tesla, Form Energy, Valar Atomics

Without venture capital, these would likely still be academic research papers or slow-moving government projects.

Proponents’ Rationale #3: Venture Capital is the Best Situated to Embrace Variance in Returns

Venture capital is the career choice for the ultimate variance seekers. In standard finance, returns often follow a normal distribution, with most outcomes clustering around the average. In venture capital, returns often follow a power law.

Because the upside of venture capital investments is theoretically infinite, but the “downside” is capped at 1x (the money invested). Venture capital firms don’t fear a 90% failure rate; they fear missing the one outlier.

This unique structure makes venture capital the best asset class for embracing variance.

For pension funds, a 50% swing in a company’s value is a disaster. For a venture capital firm, high variance is a signal of disruption. If a market is stable and predictable, there is no room for a startup to capture massive value. Venture capitalists look for tectonic shifts that create high-variance environments where new giants can be born.

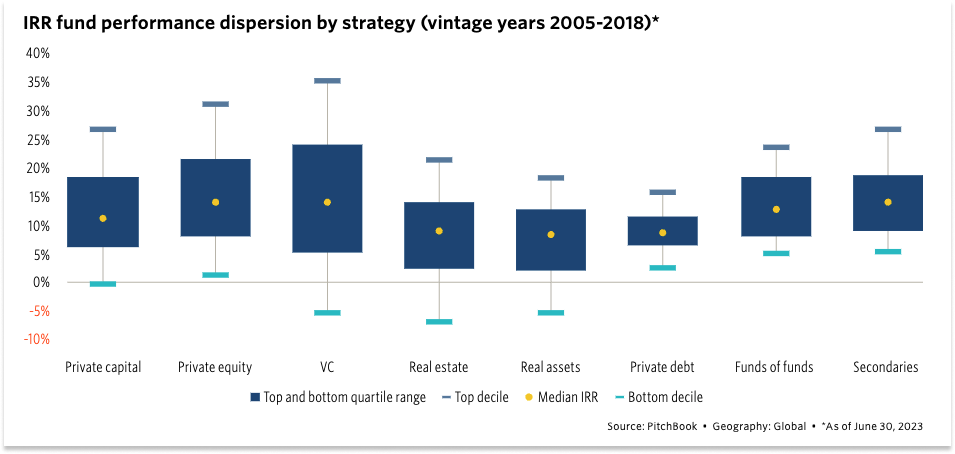

As you can see in the visualization below, the range in venture capital fund returns is much larger than for any other asset class, followed by other private speculative asset classes like private equity, private capital, and real estate.

Credit Not Boring

Consider the current AI bubble. Venture capitalists are investing billions of dollars in companies offering models, wrappers, and outrageous promises of world-changing solutions. Billions of this will undoubtedly be worth nothing very soon—not all companies are born to succeed. Why is this the current situation? Venture capitalists can’t perfectly predict which investments will succeed, so they need to cast a broad net and embrace greater return variance.

Packy provides his perspective, “Would returns look better if VCs simply funded the good companies and didn’t fund the bad ones? Maybe in the short-term, maybe not in the long-term, but it’s a moot point, because no one knows what the great ones are going to be ahead of time. Venture is beautiful for embracing that.”

Proponents’ Rationale #4: Venture Capital is Able to Fund the Wildest Ideas in the World

Venture capital is often described as the fuel for the future because it operates on a logic that most traditional financial institutions, like banks, simply can’t touch.

Most businesses are built to be stable and profitable. Venture-backed startups, however, are built for extreme outcomes. They only need one Uber or SpaceX to make their entire fund a success; they are incentivized to take massive risks on unproven technology in pursuit of large gains. Packy explains further:

Venture capitalists are willing to fund companies creating new technologies even if those companies don’t seem to have a viable business model in sight. The best venture capitalists try to fund companies that marry new technology with viable business models, but some technologies are just too early to make any economic sense. That’s OK! There are venture capitalists willing to fund those, too.

For startups, there is a period known as the valley of death, signifying the gap between an invention and a finished product. It often requires millions of dollars in research and development before a single cent of revenue is generated. From Packy, “Who’s going to fund that experimentation period? A bank? The public markets? Nope. Venture capitalists.”

Venture capitalists can fund the wildest ideas in the world, some of which will work, most of which won’t. Packy ends his thought well:

I’d argue that even if venture capital underperformed other asset classes, generated 0% returns or something, it would be a net benefit to society to have a pool of capital that funds crazy experimentation. But this is capitalism, and returns are what keeps the machine humming. So the fact that VC has generated such strong returns over a long time horizon is key.

Proponents’ Rationale #5: The Venture Capital Industry Builds Upon Itself Over Time

The venture capital industry isn’t just a series of bets; it’s a compounding infrastructure of innovation.

When people think of venture capital, they often focus on the unicorn investments—the big wins. However, the real engine of the industry is the collective learning curve generated by the vast majority of companies that didn’t make it.

Most cutting-edge technologies are too early when they first launch and go through several “winters.” Early venture capitalists fund the pioneers who often go bust because the timing is off, the hardware is too expensive, or the market isn’t ready.

However, in the grand scheme of history, those failures aren’t everything. They leave behind trained engineering and founding talent who know exactly what doesn’t work, codebases and research that become the baseline for the next venture, and the beginnings of consumer education to promote future adoption.

To be clear, venture capital firms aren’t being altruistic. They’re greedy for the “big win”, trying to get an early investment stake in the next big thing at a low price. Their risk appetite serves as an R&D subsidy for the rest of the world.

Packy, in a recent article, stated, “There seems to be collective intelligence at play on longer timescales. The opportunity to generate returns today might not exist if someone hadn’t been willing to lose money decades ago. No venture capitalist does this altruistically – they’re driven by the small, against-all-odds chance that this too-early technology might be the next big thing – but in their mistakes they create opportunity for others.”

Proponents’ Rationale #6: The Failure of One Company’s Returns Doesn’t Necessarily Spell Failure for the Fund’s Returns

More often than not, venture capital investments don’t pan out. Within a typical venture capital fund of 20-40 companies, the outcome distribution tends to look like the following:

60-70%+ Fail: These companies either go bankrupt or return less than the original investment. These bets didn’t pan out—but as we’ve discussed, they’ve laid the foundation for future companies.

20-30% Average Returns: These companies survive and might return 1-3x the investment. They are successes on paper, but don’t move the needle much for a venture capital fund.

5-10% Power Law Winners: The goal is for one or two companies in the portfolio to be “home runs” that return 10x, 50x, or even 100x the initial investment.

When developing their portfolios, venture capitalists often don’t diversify to lower risk; they diversify to increase the probability of hitting a power law winner. If you invest only in 3 companies, your chances of missing the “next big thing” are very high. The more companies you invest in, the more you increase your chances of luck.

In this way, the failure of a single company is often a planned casualty in the pursuit of the outlier.

This effect is magnified for limited partners (people and funds that invest in venture capital funds). They diversify their investments across venture capital, private equity, real estate, and other asset classes. Packy elaborates:

From the LPs’ perspective, venture capital is a small but growing high-risk / high-reward piece of a much larger portfolio. If any individual investment that one (or multiple) of their venture managers make fails, no matter how spectacularly, it’s unlikely to have a big impact on the overall portfolio. What’s more important to LPs is that venture as an ecosystem continues to take the kinds of risks that have a shot at driving higher returns.

Proponents’ Rationale #7: Venture Capital Investors Have an Active Involvement in Value Creation

There’s a common viewpoint that venture capitalists (and private equity, for that matter) are simply “money men.” However, this is a common misconception. As venture capital continues to grow in terms of the number of funds, fund sizes, and competition, venture capital firms must find ways to differentiate themselves.

To win the best deals, venture capitalists must prove they add value to a business. In most cases, this includes active support that helps the startup scale faster or more efficiently than it could on its own.

For example, most lead investors take a seat on the company’s Board of Directors. This isn’t just about oversight; it’s about providing a perspective that founders, who are deep in the daily grind, might miss, given their extensive industry experience and investing in similar companies.

Venture capitalists have seen hundreds of companies succeed and fail. They can spot patterns months before it becomes a crisis. Additionally, they can help prepare the company for an IPO or an acquisition years in advance, ensuring the financial reporting and corporate structure are ready.

To compare the two types of investors, passive investors (e.g., those invested in public stocks) and active venture capital investors, passive investors often rely on public filings or quarterly disclosures, whereas active venture capital investors have information rights and real-time data.

Similarly, passive investors generally have no say in daily operations, often voting by proxy or through regularly scheduled cadence. In contrast, venture capital investors often collaborate on hiring, pivots, pricing, and much more.

Proponents’ Rationale #8: Venture Capital can Help Social and Economic Impact

Venture capital is often benchmarked using internal rate of return and unicorns, but its impact on society and the economy is far more structural.

The Information Technology and Innovation Foundation found that between 2018 and 2022, venture capital-funded firms accounted for just 0.2% of all U.S. firms but employed 12.5% of the workforce.

Unlike traditional small businesses that grow linearly, venture capital-backed companies are designed to scale exponentially. This requires hiring hundreds (if not thousands) of high-skilled workers in a matter of months, with a significant economic impact. For every direct job created at a startup, research estimates 1.5-2.0 indirect jobs are supported in the surrounding ecosystem, from lawyers to accountants to doctors to janitors.

Venture capital companies don’t just contribute to the economy by filling jobs; they also constitute around 50% of all U.S. public companies and 77% of the total market capitalization. During economic downturns, such as the 2008 economic crisis, venture capital companies maintained positive, high-growth employment rates.

Venture capital offers a unique solution for many companies, especially compared to traditional small-business bank loans. The risk profiles differ: banks require collateral and steady cash flow, whereas venture capital firms accept total-loss risk for high-growth potential.

Bank loans help stabilize the local economies, while venture capital firms disrupt and expand the national economy. More commonly, bank loans and other small business financing primarily have a social impact on individual livelihoods and small communities. Compared with other funding sources, venture capital can fund ideas that affect nations and the world (mRNA vaccines, EVs, etc.).

Venture capitalists are often the only entities willing to fund businesses with large social impacts. Furthermore, the venture capital industry is increasingly deploying capital to break down historical barriers to entry, with notable increases in funding for female-founded and minority-led startups.

This has led to the development of a special class of venture capital investors dubbed “impact investors,” whose primary goal is to fund projects with a large impact on the world around them.

___

Packy arguably says it best, “All I’m saying is that as an asset class, venture capital is way better than it gets credit for. There’s no other asset class that’s been as positive-sum or cooked more free lunches over the past half century.”

Is Venture Capital the “Best” Asset Class?

I’ve often found it difficult to objectively determine whether something is truly the “best” among its class.

In many ways, venture capital is better than other asset classes. In others, it’s simply on par. In some categories, it underperforms. In aggregate, I would argue that venture capital is a very good asset class.

Unfortunately, there are some aspects that are hard to get past, namely, the necessity on other classes to function and return money to limited partners, the tendency to adopt a winner-take-all model where the best funds continue raising larger and larger funds and the rest of the industry struggles and dies, and the lack of liquidity and transparency for limited partners narrowing the types and profiles of potential investors and future opportunities they are interested in pursuing in the industry.

By no means is this a comprehensive analysis of every pro and con of the venture capital industry—please let me know what I’m missing, and there may be a sequel with an updated perspective given new information.

That’s a wrap on this deep dive.

Found this analysis valuable? The best way to support Brainwaves is to share it with someone who’d benefit from these insights.

Drew Jackson

Founder & Writer

Refer a Friend

Building this community has been one of the most rewarding parts of writing Brainwaves. If you know someone who’d enjoy these weekly deep dives, I’d love it if you could share your unique referral link with them. You’ll earn tangible rewards for growing our community, and they’ll get content worth their time. Win-win.

Keep Exploring

Next Deep Dive: Public vs. Private Space - May 13th, 2026

This Saturday: Weekly roundup of breaking developments across energy, space, venture capital, economics, intellectual property, and philosophy

Previous Editions: View the archive here

Stay Connected

New to Brainwaves? Join hundreds of readers getting bi-weekly deep dives into the forces reshaping our world.

Sponsor This Newsletter: Reach an engaged audience of forward-thinking readers. Email us for details.

Disclaimer: Views expressed are personal opinions, not financial advice. This content is educational only. Investment decisions carry risks - always consult professionals and do your own research. All sponsorships are clearly disclosed.

© 2026 Brainwaves. All rights reserved.