Opponents: Is Venture Capital the Best Asset Class?

Why the “Best Asset Class” is Often a High-Stakes Mirage

Credit Stanford Graduate School of Business

Roughly 90% of all startups fail. In any other industry, those odds would signal a catastrophe; in venture capital, they are simply the cost of doing business. While proponents call it the ultimate engine of innovation, a growing chorus of opponents argues that the ‘best asset class’ is actually a high-stakes gamble where most players leave the table empty-handed.

This Week’s Focus: Venture Capital

What You’ll Understand: Opposing Viewpoints on the Venture Capital Industry

Reading Time: 18 minutes for full analysis + key takeaways highlighted throughout

Key Question: Is venture capital the best asset class?

My Take: Many investors, both within and outside the industry, claim that venture capital is the best asset class. However, their opponents cite high risk, large-scale failures, reliance on external factors, and many other factors for why this simply can’t be the case. Honestly, their case has quite a bit of merit, but it may not outweigh the positives (coming in part 4).

Quick Context: This deep dive connects to my work historically on venture capital (here). New to Brainwaves? We explore the forces reshaping our world across venture capital, energy, space, economics, intellectual property, and philosophy. Subscribe here for bi-weekly deep dives plus weekly current events.

Refer a Friend - Earn These Rewards

Let’s dive in.

Venture capital has rapidly evolved and expanded throughout the last couple of decades into a full-fledged industry. Throughout its development, many of the industry’s core characteristics and the players’ fundamental properties have changed drastically to adapt to emerging trends and ultimately increase success rates.

As such, our knowledge of modern industry principles and practices may miss key developments or be fundamentally skewed by historical thinking.

The purpose of this essay today is to continue acknowledging and addressing aspects of the modern venture capital industry and any misconceptions we may have, revolving around one of the biggest overarching questions: Is venture capital the best asset class?

View part 1 and part 2 of this series.

Is venture capital truly the best asset class?

There are thousands of proponents and opponents of the venture capital industry. On one hand, there are thousands of companies and founders that use venture capital funding to change the world and get rich in the process. On the other hand, this comes at the expense of LPs, company failures, and reliance on other factors.

Today, our goal is to understand the main arguments of these naysayers, those who habitually oppose and are skeptical of the industry’s true value. Part 4, the final piece of this series, will present the champions’ viewpoint.

The Opponents

The opponents of venture capital being the best asset class list a wide variety of reasons, the main of which are:

Venture capital is incredibly risky and has a high failure rate

Venture capital funds are very illiquid

Venture capital returns are highly variable with a high dependence on “home runs”

Venture capital firms charge high fees (2 & 20)

There are substandard and unqualified investors in venture capital

Venture capital firms make money when other people do all the hard work

Many venture capital funds are struggling

Because venture capital firms invest in private companies, there can be a lack of transparency for limited partners

Venture capital requires larger, more mature asset classes for its exits—venture capital can’t exist in a vacuum

Opponents’ Rationale #1: Venture Capital is Incredibly Risky and Has a High Failure Rate

Just because you received a venture capital investment does not mean you’re going to be the next unicorn (although it doesn’t hurt your chances). In fact, in venture capital, risk isn’t just a possibility—it’s at the core of the business model.

Roughly 90% of all startups fail. Venture capital’s goal is to find and invest in the 10% that don’t fail (or have less likelihood of failure). In practice, this often means investing in companies with high potential but high failure rates.

Packy at Not Boring summarizes the problem well: “No asset class’ constituents fail at a higher rate than venture capital’s, yet venture capital’s returns match or exceed all the others’... Even the best venture funds are wrong much more often than they’re right.”

Venture capital sits at a unique point on the risk-return spectrum, taking many risky bets with the hope that a small few will return well enough to cover the others and then some. If the failure rate is so high, why do institutional investors (e.g., pension funds and insurance companies) continue to invest in venture capital?

Like other private markets, venture capital often moves differently than the stock market, providing an uncorrelated return profile that enables further portfolio diversification.

Additionally, these investors want access to the home run upside. In venture capital, you can only lose 1x your money on a failure (which is often the case), but it provides an opportunity to make 100x or even 1000x on a success.

On the whole, these factors create dynamics where the best funds, those hitting home runs consistently, rise to the top percentiles, while the majority of funds, those consistently striking out, struggle and eventually disappear.

Opponents’ Rationale #2: Venture Capital Funds are Very Illiquid

Packy states the issue perfectly, “There are many good reasons for LPs (limited partners, the people and institutions who invest in funds) to be avoiding venture right now. Most of them boil down to one thing: liquidity.”

Traditionally, venture capital funds were designed to be ~10-year vehicles, with the first 5 years for investing the money and the other 5 for building and selling companies. Thus, as an investor, your money is tied up for 8-10 years before you begin to see money back and any capital gains.

In 2026, this timeline can often be longer, as funds are hesitant to deploy capital on the frontend and companies are staying private longer, resulting in 10-15-year fund timelines that further increase the illiquidity of these funds.

This means many funds are reaching their legal expiration date while still holding most of their assets. As a result, fund extensions have become increasingly popular to ensure capital can be recovered.

The “J-Curve” represents a fund’s return profile and its illiquidity. In the first few years, a fund’s value drops because of management fees and early investment failures. It only curves upward in the final years of the fund’s lifecycle as the winners grow and eventually exit.

For many funds, limited partners don’t give the venture capital firm all of the money at once. Instead, they are “called” over several years, meaning the investor must keep that cash ready but relatively unproductive until the venture capital firm asks for it, further compounding the lack of immediate returns for investors.

Therefore, an investor might not see a single dollar of distributions (profit) until year 7 or 8 of the investment. Because this illiquid wait time has become so long, the industry has developed new ways to artificially create liquidity before a company actually goes public or is acquired.

In 2025, the global secondaries market reached $240M. This market enables limited partners to sell their stakes in a fund to another investor, or for founders to sell a portion of their shares to specialized firms.

Additionally, if a venture capital firm has a great company but its fund is expiring, they might “sell” that company into a new fund they also manage. This gives old investors a choice: take their cash now or roll into the new fund to keep waiting for a bigger exit.

It’s a very difficult environment for venture capital investors right now. Limited partners need returns to fund their insurance programs, pension funds, university research, and other activities. They can easily sell stocks and bonds at their market value; they can’t sell their venture capital stakes as easily. So it’s not surprising some limited partners are becoming hesitant to provide capital for venture capital firms.

Opponents’ Rationale #3: Venture Capital Returns are Highly Variable, With a High Dependence on “Home Runs”

Peter Thiel, in his book Zero to One: Notes on Startups, or How to Build the Future, states:

The error lies in expecting that venture returns will be normally distributed: that is, bad companies will fail, mediocre ones will stay flat, and good ones will return 2x or even 4x. Assuming this bland pattern, investors assemble a diversified portfolio and hope that winners counterbalance losers. But this “spray and pray” approach usually produces an entire portfolio of flops, with no hits at all. This is because venture returns don’t follow a normal distribution overall. Rather, they follow a power law: a small handful of companies radically outperform all others. If you focus on diversification instead of single-minded pursuit of the very few companies that can become overwhelmingly valuable, you miss those rare companies in the first place.

One of the best parts of venture capital is that not all investments need to pan out, enabling them to take risky bets that other asset classes cannot.

Due to these factors, venture capital firms are often reliant on a few core investments (usually unknown from the start but identified throughout the investment lifecycle) to return the majority of their capital and profit.

However, if you don’t manage to capture any of those home-run performers, your fund struggles—as many do today. This can lead to competent, powerful investors failing solely because of the field’s uncertainty, potentially decreasing capital available to companies in the future. Thiel continues:

Of course, no one can know with certainty ex ante which companies will succeed, so even the best VC firms have a “portfolio.” However, every single company in a good venture portfolio must have the potential to succeed at a vast scale.

Opponents’ Rationale #4: Venture Capital Firms Charge High Fees (2 & 20)

The traditional compensation structure for venture capital and private equity funds is known as the “2 and 20” structure. On the surface, it sounds simple, yet it creates a powerful set of incentives that dictate how money is invested and managed.

The “2” refers to the annual management fee (usually 2%), calculated based on the total capital committed to the fund, not the amount currently invested. The purpose is to keep the fund afloat by paying salaries, covering office space, travel, technology, legal expenses, and more.

For some quick math, if you raised a $1B fund, you would receive 2% in annual management fees, or $20M. Over a typical 10-year fund life, that’s $200M in guaranteed revenue, regardless of whether the fund makes a single dollar in profit.

Granted, most modern funds include a “step-down” provision where, after the initial investment period (3-5 years), the fee might drop to 1.5% or 1% as the workload shifts from finding new deals to simply managing existing ones.

The “20” refers to the performance fee, and it’s where venture capital firms make their real wealth. Once the fund has returned all the original capital to the limited partners, the general partners retain 20% of any additional profits. This is designed to ensure the venture capital fund only gets rich if the investors get rich.

If our $1B fund returns $4B (once all investments are exited), the limited partners receive $1B back first, and the remaining $3B is divvied up: 80% to the investors and 20% to the venture capital firm.

Over the last few years, a clear divide has emerged in the industry. As a new class of funds emerges, dubbed “megafunds”, with over $10B in assets under management. For these firms, the management fees ($200M+/year) are so massive that the partners are wealthy even if the fund’s performance is mediocre. Smaller, scrappier funds, usually $500M and under, must hit home runs to survive, as their management fees barely cover basic operations.

Thus, some firms are more heavily incentivized to carefully select and pursue home-run investments, even if the economics (2 & 20) remain the same.

Overall, investors generally accept high fees so long as the fund provides alpha (returns higher than what the investor could earn elsewhere, usually the stock market). When performance dips, these fees are among the first things limited partners seek to renegotiate.

Opponents’ Rationale #5: There Are Substandard and Unqualified Investors in Venture Capital

Despite its elite reputation, venture capital is a highly fragmented industry. In 2026, the gap between top-tier firms and “unqualified” investors has never been wider.

When observers or critics speak of “substandard” or “unqualified” investors, they are usually referring to three types of venture capital players that can actually damage a startup’s health:

The Hype Chaser: These are investors, often retail groups, family offices, or non-tech corporations, who enter venture capital only during the boom times. Unfortunately, they often lack the stomach for the 7-10 year startup winter. When a company faces volatility or uncertainty, these investors are often the first to panic and push for a premature sale, at the company’s long-term detriment.

The Dumb Money: These are capital providers that provide zero strategic support. While an elite venture capital firm provides hiring assistance and customer introductions, an unqualified investor might overcomplicate the cap table, demanding toxic terms that make it impossible for the founder to raise more money later, or require excessive hand-holding, wasting management’s time instead of finding ways to add value.

The Ghost Investor: Ghost investors are groups that have stopped writing checks but still want to appear active, a significant red flag in today’s climate. If an existing investor doesn’t follow on in your next round, it sends a signal to the rest of the market that something could be wrong with your company. Many “unqualified” investors often run out of dry powder but don’t tell the founder until it’s too late.

Based on the above explanation, you may have come to the natural conclusion that “substandard” or “unqualified” investor types are detracting from the industry, and should be eliminated—that was my first thought, too. Packy provides some clear commentary on this point:

They stand in the way of acquisitions that would be life-changing for founders but meaningless for returns. Often, the most helpful thing some VCs can do is write a check and get out of the way. I’ve worked with bad ones from the other side of the table and I know how harmful they can be. The good news is, over time, the market typically punishes the bad ones.

He continues with a counterintuitive point:

If you zoom in on the behavior of any one participant at any given time, you might think that they’re behaving stupidly. In many cases, they are. The ecosystem works not in spite of, but because of, the stupidity of some of its participants.

There are undoubtedly investors who show up to work and do a substandard job, as you would find in any career. Unfortunately, in this case, all suffer. In what ways can this be prevented?

Arguably, the biggest reason behind this trend is the lack of formalized training and oversight of venture capitalists—there’s technically a very low barrier to entry.

Additionally, the industry is moving toward structural and technological safeguards to weed out low-quality investors. The goal is to shift from a traditional handshake culture to a data-driven culture where poor performance and toxic behavior have immediate consequences.

For instance, founders have begun to vet venture capital firms as rigorously as venture capital firms are vetting them. This includes asking for references from successful and unsuccessful portfolio investments to discover how the investor behaves when things go right and wrong.

Review sites are gaining traction, allowing founders to leave reviews for venture capitalists and flag sub-performers, helping future founders understand the scope of their potential partnership.

Lastly, the National Venture Capital Association and similar entities have launched initiatives to increase transparency across the venture capital process. A main initiative is creating open-source, fair-market-term sheets that enable founders to recognize unfair terms as red flags for unqualified investors.

Opponents’ Rationale #6: Venture Capital Firms Make Money When Other People Do All the Hard Work

The argument that venture capitalists make money while others do the work is a common critique of the industry and has some merit. Underlying the argument is the fundamental tension between capital (in this case, the venture capital firm’s capital) and labor (the founders’ and employees’ “sweat equity”).

At the very beginning, a company’s value is essentially zero. Founders and early employees provide 100% of the labor, but they often lack the resources to significantly scale. In many cases, the solution is to bring in a venture capital firm to provide some of the capital necessary to grow and achieve future projections.

In return, a founder trades a portion of their ownership (often 20-40%+) for the capital needed to hire a team and build the product. Fast forward to exit, if the company sells for $1B, a venture capital firm that owns 20% makes $200M. Critics will argue that the venture capital firm didn’t write the code, sell the product, or pull late-nighters to ensure viability—yet they took a massive share of the value created by those who did.

The counterargument used by the venture capital industry is based on the nature of the risk each party assumes. For the founder, if the startup fails, they lose years of their life and potential salary, but they often don’t lose millions of their own dollars. In contrast, if the startup fails, the venture capital firm loses its entire investment. As such, there is an asymmetry in the risk taken (in the venture capital firm’s opinion), which justifies the compensation received on successful investments.

Recently, this paradigm has been shifting in favor of the founder. Founder-friendly terms are appearing more often in term sheets, including “super-voting shares” that allow founders to keep control of the company’s direction even if they own a minority of the stock.

Additionally, to help prevent founders from burning out while venture capitalists wait for a massive exit, many term sheets include provisions that allow founders to sell a small portion of their shares in a secondary transaction early in the venture. This allows the founders to get paid for their hard work before the investor gets their final payday.

Separately, some venture capital firms are moving away from passive investing towards the creation of venture studios, where the venture capital firm actually provides the first engineers, designers, and recruiters. In these cases, the work and value-creation process is more evenly shared between the firm and founders, justifying the return profiles.

Opponents’ Rationale #7: Many Venture Capital Funds are Struggling

In March 2026, the Chairman of the 45th Annual Small Business Forum summarized this issue well: “This panel will also examine trends of increased concentration in the venture capital industry. For example, in the first seven months of 2025, roughly 40% of all venture capital dollars flowed to just 10 companies, while the share of deals below $5 million fell to a decade-low of 49%. On the fundraising side, thirty firms accounted for approximately seventy-five percent of the total venture dollars raised in 2024.”

Now, to be clear, concentration doesn’t exactly mean many venture capital funds are struggling, just that some are outperforming the rest.

Carta, a software to manage equity management, estimates that from 2021 to 2024, the number of new venture capital funds raised fell by 68%. In the same period, the annual count of investors who made at least one new investment in a U.S.-based startup declined by 26%.

Often, one of the biggest signs of a successful venture capital firm is the ability to raise subsequent funds, usually at larger fund sizes.

Through these metrics—concentrated funds raising the majority of venture dollars and a decrease in firms raising new funds—it’s a pretty sure bet that many venture capital funds are struggling.

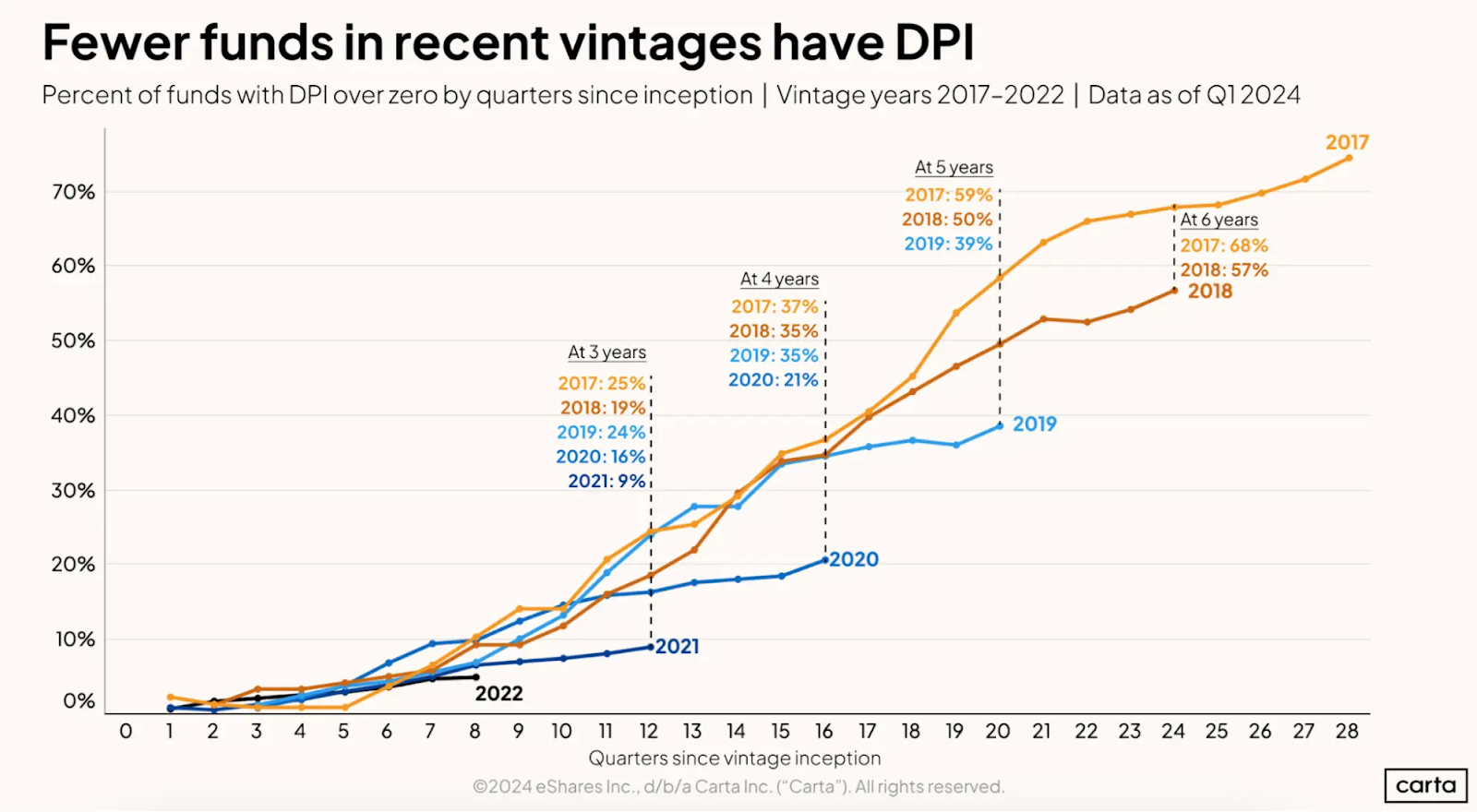

In recent years, limited partners have struggled to earn significant returns on their venture capital fund investments. This is measured by a metric known as distributed-to-paid-in capital (DPI), which compares the cash returned to investors with the capital they contributed.

Among the most recent venture capital fund vintages, DPI has been hard to achieve. Carta estimates that just 21% of funds from the 2020 vintage have generated any DPI for investors thus far, compared to 37% over the same period for 2017 vintage funds. They include the following graph, which illustrates this point well:

In the late 2010s and early 2020s, there was a surge of new venture capital funds as investors sought to capitalize on a growing market. Thus, many speculate that the current trends of the shrinking VC landscape represent a normalization back to long-term trends.

Aside from these factors, the recent market consolidation is painful for many funds, resulting in fewer fundraising opportunities for both less-experienced founders and newer investors.

Opponents’ Rationale #8: Because Venture Capital Firms Invest in Private Companies, There Can Be a Lack of Transparency for Limited Partners

In most cases, the relationship between the general partner of a venture capital fund (the person managing the investments and portfolio day-to-day) and the limited partner (the institution or individual(s) providing the money for the fund) is often a black box.

Because venture capital invests in private companies, they aren’t subject to the same public disclosure rules as a company listed on a public stock exchange. This creates a significant information asymmetry.

In the public markets, a stock price is updated every second. In venture capital, the value of a company is often a “best guess” based on the last time someone wrote an investment check. For instance, a company might have raised money at a $1B valuation in 2021. If the market crashes in 2022, the venture capital firm might still carry that company at $1B on its books until it raises additional capital in a down round or exits.

Even though limited partners are the primary financiers, they rarely have a seat on the startup’s board. Limited partners usually receive quarterly portfolio summaries. They might see “Company X is doing well,” but they won’t see the internal Slack messages, customer data, board minutes, or the granular monthly burn rate.

This is especially the case if the limited partner also invests in competitors of the company, in which case, general partners must strictly limit what information they pass up the chain to prevent trade secrets from leaking.

However, limited partners have begun to push back, wanting increased transparency. For example, in 2026, the Institutional Limited Partners Association introduced new reporting templates that force venture capital firms to provide more granular data on fees, expenses, and performance metrics. In another instance, California recently passed a diversity law requiring venture capital firms to report the demographic data of the founders they fund—moving transparency from financials to include social and operational metrics.

Opponents’ Rationale #9: Venture Capital Requires Larger, More Mature Asset Classes For Its Exits—Venture Capital Can’t Exist in a Vacuum

Venture capital doesn’t exist in isolation within the financial landscape. It is often the on-ramp for companies to a much larger global financial highway. While venture capitalists specialize in high-risk, early-stage growth, they cannot survive unless they can eventually hand their companies off to larger, more mature asset classes to provide liquidity.

As we’ve discussed, venture capital creates value, though it’s largely paper value until an exit. For venture capital to return cash to its investors, it needs a buyer with significantly deeper pockets, typically from three mature asset classes.

Firstly, the public markets are the ultimate destination for startups. When a company lists on an exchange, it gains access to a pool of capital valued at trillions of dollars from retail and institutional investors. JP Morgan estimates that this accounts for around 10-15% of all venture capital exits.

Secondly, large strategic incumbents (e.g., Google, Microsoft, and Costco) regularly use their cash reserves to acquire companies. For example, in 2026, the race to build AI infrastructure has led many strategics to record-breaking M&A deal values and volume, with these giants serving as exit opportunities for smaller innovators. Sales to larger strategic players represent around 50-55% of all venture-capital backed exits, the largest channel.

Lastly, large financial institutions (e.g., private equity firms, family offices) deploy significant capital to continue growing these companies for years to come. These investors often bring significant operational, technological, and sector-specific expertise through prior investments. Financial investors account for the remaining 25-40% of venture capital investment exits.

Venture capital relies on these larger asset classes to achieve liquidity and to ensure the next stage in the company’s growth lifecycle (traditionally, a more mature, moderate-growth stage).

However, this has become harder recently. In 2026, Stanford Professor Ilya Strebulaev found that the average time to exit was between 6 and 10 years, with this timeframe increasing steadily over the last 3-5 years. Only 35% of companies exited within 1-5 years, 40% within 6-10 years, and 25% within 11-15 years.

Because companies are staying private longer, the secondary market has become vital. This capital allows early investors and employees to sell some or all of their shares to other private investors before the company actually fully exits.

This provides a pressure-release valve for the venture capital ecosystem, ensuring capital keeps flowing even when the IPO or M&A windows aren’t favorable.

Part 4 to come next.

That’s a wrap on this deep dive.

Found this analysis valuable? The best way to support Brainwaves is to share it with someone who’d benefit from these insights.

Drew Jackson

Founder & Writer

Refer a Friend

Building this community has been one of the most rewarding parts of writing Brainwaves. If you know someone who’d enjoy these weekly deep dives, I’d love it if you could share your unique referral link with them. You’ll earn tangible rewards for growing our community, and they’ll get content worth their time. Win-win.

Keep Exploring

Next Deep Dive: Proponents: Is Venture Capital the Best Asset Class? - April 29th, 2026

This Saturday: Weekly roundup of breaking developments across energy, space, venture capital, economics, intellectual property, and philosophy

Previous Editions: View the archive here

Stay Connected

New to Brainwaves? Join hundreds of readers getting bi-weekly deep dives into the forces reshaping our world.

Sponsor This Newsletter: Reach an engaged audience of forward-thinking readers. Email us for details.

Disclaimer: Views expressed are personal opinions, not financial advice. This content is educational only. Investment decisions carry risks - always consult professionals and do your own research. All sponsorships are clearly disclosed.

© 2026 Brainwaves. All rights reserved.